Printable Indiana St 105 Form

Indiana St 105 Sample

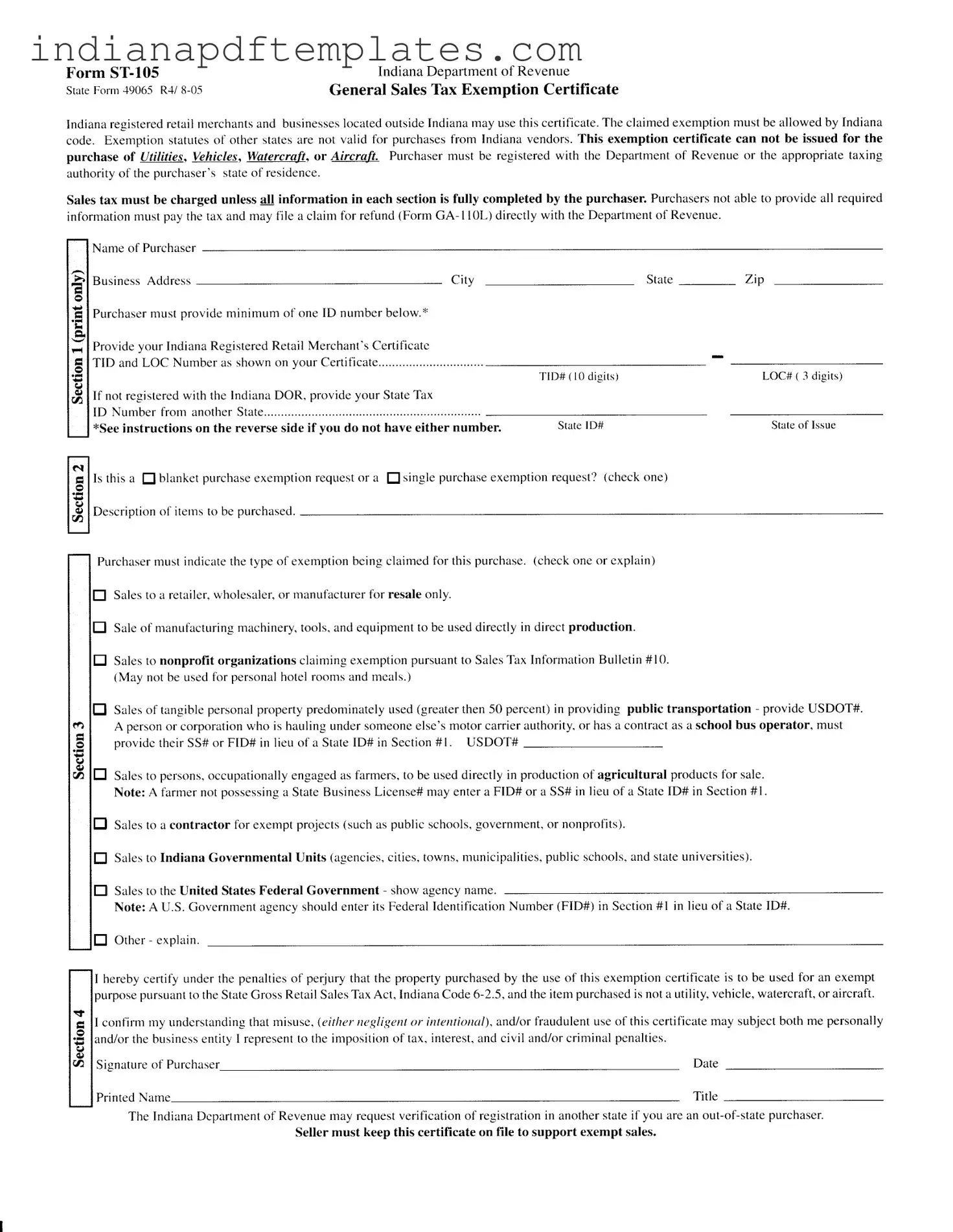

Form |

Indiana Department of Revenue |

StateForm :19065 |

General SalesThx Exemption Certificate |

Indianaregisteredrelail merchantsand businesseslocatedoutsideIndianamay usethis certificate.The claimedexemptionmust be allowedby Indiana code. Exemption slatutesof other statesare not valid tbr purchasesfrom Indiana vendors.This exemption certilicate can not be issued for the purchase of lLili/iqg, Vehicles, Watercraft, or Ai/crafr. Pttrcha.sermust be registered with the Depafiment of Revenue or the appropriate taxing authorityofthe purchaser'sstateof residence.

Sales tax must be charged unless a!! information in each 6ection is fully completed by the purchaser. Purchasersnot able to provide all required informationmust pay the tax and may file a ctaim for refund(Form GA- I

Name of Purchaser

B u s i n e s s A d d r e s s |

C i t y |

P u r c h a s e rm u s t p r o v i d e m i n i m u m o f o n e I D n u n i b e r b e l c l w . t '

Provide your Indiana Registered Retail Merchant's Certificatc TID and LOC Number as shown on your Certificate .

If not registered with the Indiana DOR, provide your State Tax I D N u m b e r f r o m a n o t h e r S t a t e . . . . . .

*See instructions on the reverse side if vou do not have either number .

State _ |

Zip |

T I D # ( l 0 d i g i t s ) |

LOC# ( 3 digits) |

SrarelD# |

Stateof Issue |

HI s t h i s a I b l a n k e t p u r c h a s ee x e m p t i o n r e q u e s to r a I

D e s c r i p t i o no f i l e m s t o b e p u r c h a s e d .

s i n g l e p u r c h a s ee x e m p t i o n r e q u e s t ? ( c h e c k o n e )

Purchasermust indicatethe lype oI exemptionbeing claimedfor this purchase.(checkone or explain)

E

E

E

E

Salesto a retailer,wholesaler,or manufacturerfor resaleonly.

Saleof manufactu ng machinery tools.andequipmentto be useddirectly in direct production.

Salesto nonprofft organizations claimingexemptionpursuantto SalesTax lnformationBullelin #10. (May not be usedfor personalhotel roomsand meals.)

Salesofrangible personalpropertypredominatelyused(greaterthen50 percent)in providing public transportation - provide USDOT#.

Apersonor corporalionwho is baulingundersomeoneelse'smotor carrierauthority,or hasa contractasa schoolbus operator, must providc their SS#or FID# in lieu of a StateID# in Section#1. USDOT# -

E

E

E

Salesto persons,occupationallyengagedasfamers, to be useddirectly in productionof agricultural productsfor sale. Note: A farmernot possessinga StateBusinessLicense#may entera FID# or a SS# in lieu of a StateID# in Section#1.

Salesto a contractor for exemptprojects(suchaspublic $chools,or nonprofits). Sovemment,

Salesto Indiana Governmental Units (agencies,cilies,towns.municipalities,public schools,and slateuniversities).

El

Salesto the United States Federal Government - show agency name .

Note: A U . S . Government asencv should enter its Federal Identification Number (FID#) in Section #1 in lieu of a State ID# .

E O t h e r - e x p l a i n .

Iherebycerlify underthe penaltiesof perjury that lhe propeny purchasedby the useof this exemptioncertificateis to be usedfor an exempt purposepursuanlto theStateCrossRetailSalesTaxAct,

Iconfirm my undeBtandingthat misuse,(?ifrer egligentor intentioral), and/orfraudulentuseofthis certificatemay subjectboth me personally and/orthe businessentity I represenlto the impositionoftax, interest,and civil and/orcriminal penalties.

Signature of Purchaser |

Date |

Printed Name |

Title |

The Indiana Dcpartntent of Revenue may request verification of registration in another state if you are an out - of - state purchaser .

Seller must keep this certificate on file to support exempt sales.

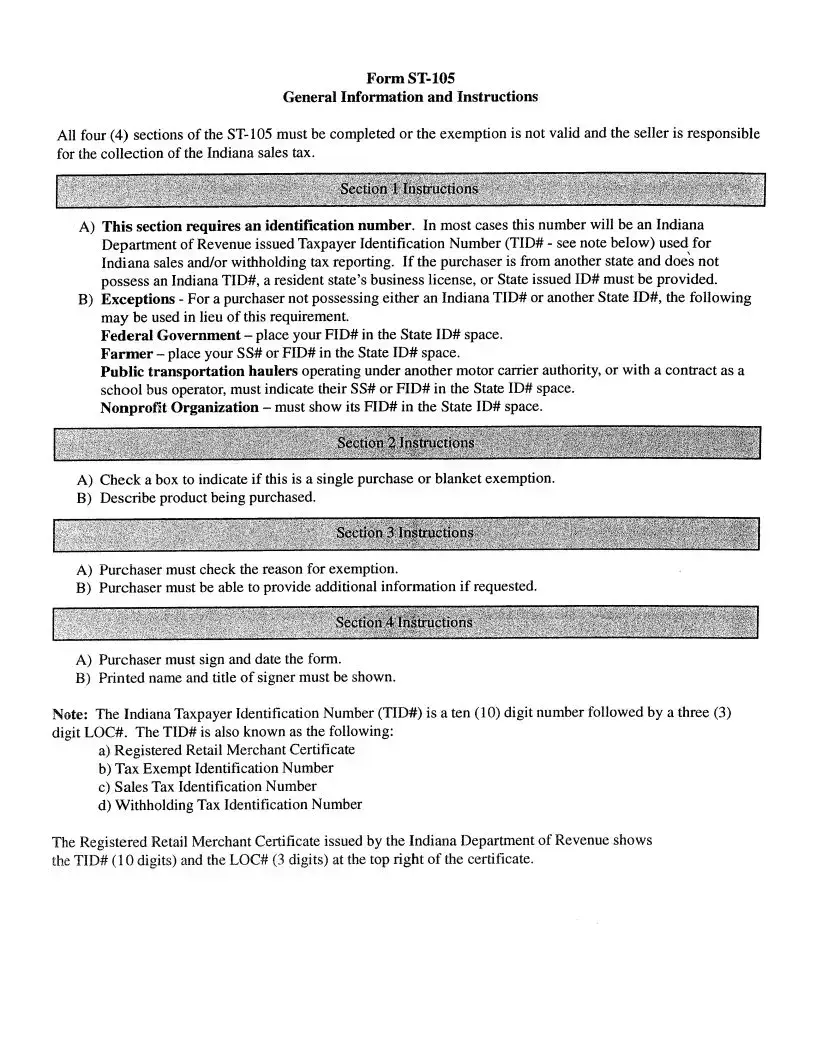

GeneralInfonnation and Instructions

All four (4) sectionsof

A)This sectionrequires an identification number. In mostcasesthis numberwill be anIndiana DeparunentofRevenueissuedTaxpayerldentificationNumber(TID# - seenotebelow) usedfor Indianasalesand/orwithholdingtax reporting. If the purchaseris from anotherstateanddoei not possessanIndianaTID#, a residentstate'sbusinesslicense,or StateissuedID# mustbeprovided.

B)Exceptions- For a purchasernot possessingeitheranIndianaTID# or anotherStateID#, thefollowing

may beusedin lieu of thisrequirement. tr'ederalGovernment- placeyourFID# in theStateID# space. Farmer - placeyour SS#or FID# in theStateID# space.

Public transportation haulersoperatingunderanothermotor carrierauthority,or witb a contractasa

schoolbusoperator,mustindicatetheir SS#or FID# in theStateID# space. Nonprolit Organization- mustshowits FID# in the StateID# space.

A)Check a box to indicateif this is a singlepurchaseor blanketexemption.

B)Describeproductbeingpurchased.

A)Purchasermustcheckthereasonfor exemption.

B)Purchasermustbe ableto provide additionalinformation if requested.

A)Purchasermust sign and date the form.

B)Printednameandtitle of signermustbe shown.

Note: The Indiana TlrxpayerIdentification Number (TID#) is a ten (10) digit number followed by a thtee (3) digit LOC#. The TID# is alsoknown asthe following:

a)RegisteredRetail Merchant Certificat€

b)Tax Exempt Identification Number

c)SalesTax Identification Number

d)Withholding Tax Identification Number

The RegisteredRetailMerchantCertificateissuedby the IndianaDepartrnentofRevenueshows the TID# ( I 0 digits) and the LOC# (3 digits) at the top right of the certificate'

File Characteristics

| Fact Name | Description |

|---|---|

| Purpose | The Indiana ST-105 form serves as a General Sales Tax Exemption Certificate, allowing registered merchants to claim exemptions on eligible purchases. |

| Eligibility | Only Indiana-registered retail merchants and businesses located outside Indiana can use this certificate. Exemptions from other states are not accepted. |

| Exemptions | This form cannot be used for purchasing liquor, vehicles, watercraft, or aircraft. Specific exemptions must be clearly indicated on the form. |

| Filing Requirements | All sections of the ST-105 must be completed for the exemption to be valid. Incomplete forms will result in the seller being responsible for collecting sales tax. |

| Governing Law | The use of the ST-105 is governed by the Indiana Code 6-2.5, which outlines the state's sales tax regulations and exemptions. |

Essential Points on This Form

What is the Indiana ST-105 form?

The Indiana ST-105 form is a General Sales Tax Exemption Certificate used by registered retail merchants and businesses located outside of Indiana. This form allows eligible purchasers to claim exemptions from sales tax on certain purchases. However, the exemption must comply with Indiana code, and exemptions from other states are not applicable for purchases made from Indiana vendors.

Who can use the Indiana ST-105 form?

Eligible users of the Indiana ST-105 form include:

- Registered retail merchants in Indiana.

- Businesses located outside of Indiana that have the appropriate tax identification numbers.

- Nonprofit organizations, farmers, contractors for exempt projects, and governmental units.

All users must complete the required sections of the form to qualify for the exemption.

What information is required to complete the ST-105 form?

To complete the ST-105 form, purchasers must provide the following information:

- Name of the purchaser.

- Business address, including city and zip code.

- Tax Identification Number (TID) and Location (LOC) number, if registered in Indiana.

- State Tax ID number if registered in another state.

- Type of exemption being claimed, such as sales for resale or sales to nonprofit organizations.

All sections must be filled out completely to ensure the exemption is valid.

What types of purchases are exempt from sales tax using the ST-105 form?

The ST-105 form can be used for various types of exempt purchases, including:

- Sales to retailers, wholesalers, or manufacturers for resale.

- Sales of manufacturing machinery and equipment used directly in production.

- Sales to nonprofit organizations under specific conditions.

- Sales of tangible personal property used in public transportation.

- Sales to government units or the U.S. Federal Government.

However, the form cannot be used for purchasing utilities, vehicles, watercraft, or aircraft.

What happens if the required information is not provided?

If the purchaser fails to provide all required information on the ST-105 form, the seller must charge sales tax on the transaction. In such cases, the purchaser may file a claim for a refund using Form GA-1106 directly with the Indiana Department of Revenue after paying the tax.

Is the ST-105 form valid for blanket exemptions?

Yes, the ST-105 form can be used for blanket exemptions. Purchasers can indicate whether they are requesting a single purchase exemption or a blanket exemption for multiple purchases. However, the description of the items to be purchased must still be provided to ensure compliance with the exemption criteria.

What are the consequences of misusing the ST-105 form?

Misuse of the ST-105 form, whether through negligence or intentional fraud, can lead to significant consequences. Both the individual and the business entity may face tax liabilities, interest charges, and civil or criminal penalties. It is essential to ensure that the form is used correctly and for valid exempt purposes to avoid these repercussions.

Misconceptions

Misconceptions about the Indiana ST-105 form can lead to confusion and potential tax liabilities. Here are six common misconceptions:

- Anyone can use the ST-105 form for any purchase. This is incorrect. The form is specifically for tax-exempt purchases allowed under Indiana law. Exemptions from other states do not apply.

- The ST-105 form can be used for any type of item. This is misleading. The form cannot be used for the purchase of vehicles, watercraft, or aircraft, among other restricted items.

- Completing only part of the form is sufficient. This is false. All sections of the ST-105 must be fully completed for the exemption to be valid. Incomplete forms do not provide tax exemption.

- Out-of-state purchasers do not need to provide any identification. This is not true. Out-of-state purchasers must provide their state tax identification number or other valid identification as specified.

- The seller does not need to keep the ST-105 form on file. This is incorrect. Sellers must retain the certificate to substantiate exempt sales and avoid tax liability.

- Purchasers can misuse the form without consequences. This is a serious misconception. Misuse of the ST-105 can lead to penalties, including tax liabilities and potential legal action against the purchaser and the business.

Find More Templates

Snap Self Employment Form - Individuals use this form to maintain accurate financial records.

When engaging in the sale or purchase of a recreational vehicle in Texas, utilizing the correct documentation is vital. One such resource is the Fast PDF Templates, which offers a user-friendly format for the Texas RV Bill of Sale, ensuring that all necessary details are accurately captured to protect both parties in the transaction.

Indiana Wh 4 - Accuracy in claiming dependents directly impacts the employee's tax liability.